Test a Business Idea with Facebook Ads (2026 Guide)

Learn how to validate your startup idea using Facebook ads on a budget. Discover targeting strategies, ad creation tips, and metrics that prove market demand.

Mar 23, 2026

AI will not replace accountants, but it is fundamentally reshaping what accountants do. While AI automates routine tasks like data entry and reconciliation, accountants remain essential for judgment, strategic advisory, compliance, and relationship management—areas where human expertise cannot be replicated.

The question keeps coming up in accounting circles, online forums, and industry conferences: will artificial intelligence eventually replace accountants entirely?

Here's the short answer: no. But that doesn't mean everything stays the same.

AI is already transforming accounting work in significant ways. It's automating repetitive tasks, accelerating reporting cycles, and changing what accountants spend their time doing. According to research from Stanford University, accountants using AI support more clients per week and finalize monthly statements 7.5 days faster than those using traditional methods.

So while AI won't replace accountants, it's definitely redefining the profession. Let's look at what's actually happening.

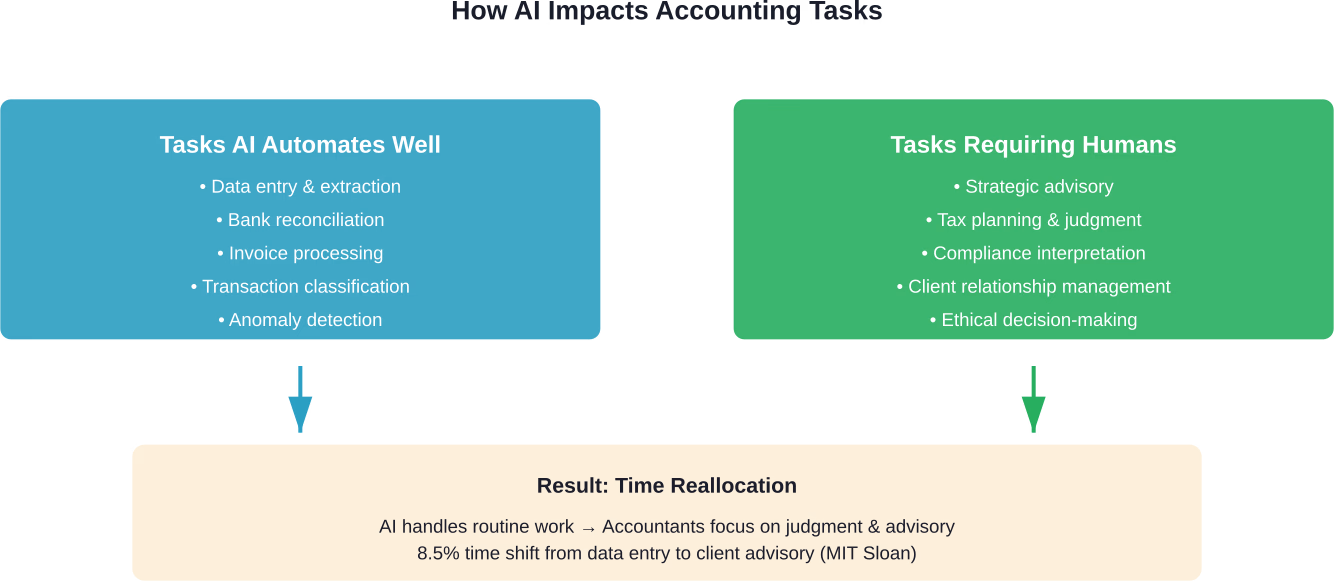

AI excels at handling routine, rule-based accounting tasks. These are areas where technology has already proven effective and continues to improve.

Data entry represents the most obvious target. Optical character recognition (OCR) technology extracts vendor names, dates, and amounts from PDFs and emails without human intervention. Fewer typos, faster month-end closes.

Bank reconciliation is another area seeing rapid automation. Software now matches transactions automatically, flagging exceptions for human review rather than requiring accountants to verify every single line item.

Invoice processing has become significantly faster. AI classifies transactions, routes approvals, and detects duplicate payments. What used to take hours now happens in minutes.

According to MIT Sloan research, AI reallocates approximately 8.5% of accountant time from routine data entry toward more complex client advisory tasks. That's not job replacement—that's task redistribution.

But here's the thing: these automation gains don't eliminate the need for accountants. They shift where accountants add value.

Some accounting work simply can't be automated, at least not with current or foreseeable AI capabilities.

Professional judgment sits at the top of this list. When should revenue be recognized on a complex multi-year contract? How should an unusual transaction be classified? These questions require understanding context, regulations, and business strategy in ways AI cannot replicate.

Tax planning represents another area where humans dominate. Sure, AI can prepare straightforward returns. But strategic tax planning—understanding how business decisions impact tax liability, navigating gray areas in tax law, optimizing structures across jurisdictions—requires expertise that goes far beyond pattern recognition.

Client relationships matter tremendously in accounting. Trust, communication, understanding client needs, providing reassurance during audits—these interpersonal elements define much of an accountant's value, especially at higher service levels.

Compliance and ethical judgment present similar challenges for automation. When regulations are ambiguous or conflicting, when ethical dilemmas arise, when professional standards require interpretation—these situations demand human decision-making.

According to the International Federation of Accountants (IFAC), professional accountants are evolving beyond compliance and reporting toward becoming strategic advisors and data guardians. That transformation is enabled by AI, not threatened by it.

Real employment projections paint a more nuanced picture than the "AI apocalypse" narrative suggests.

The U.S. Bureau of Labor Statistics projects total employment to grow from 170.0 million in 2024 to 175.2 million in 2034, an increase of 3.1 percent. While this represents slower growth than the previous decade, it's still growth.

For accountants specifically, the BLS Occupational Outlook Handbook notes that completing certification in specialized accounting fields, such as becoming a licensed Certified Public Accountant (CPA), may improve job prospects. The projected median annual wage for accountants and auditors in 2026 ranges from $75,000 to $110,000 for senior roles, with staff accountants earning between $60,000 and $75,000.

Here's what matters: the BLS explicitly incorporates AI impacts into employment projections. According to their methodology, AI is expected to primarily affect occupations whose core tasks can be most easily replicated by generative AI in its current form. Accounting involves a mix of automatable and non-automatable tasks, which moderates overall impact.

Research from Brookings on workers' capacity to adapt to AI-driven job displacement found that among workers in the top quartile of occupational AI exposure, 26.5 million have above-median adaptive capacity. However, 6.1 million workers (4.2% of the workforce) face higher vulnerability due to lower adaptive capacity.

The takeaway? Job displacement risk exists, but it's concentrated and manageable, not universal.

The real story isn't replacement—it's role evolution.

Traditional bookkeeping tasks are declining as a percentage of what accountants do. Data entry, manual reconciliation, basic transaction recording—these activities are being automated aggressively.

Advisory services are expanding proportionally. Financial analysis, forecasting, business strategy support, process improvement recommendations—these higher-value activities are consuming more of accountants' time.

According to AICPA research, finance teams still dedicate 65% of report outputs to hindsight reporting through descriptive and diagnostic methods, while predictive and prescriptive analytics remain underutilized. That gap represents opportunity for accountants who develop analytical skills.

Technology management is becoming part of the accountant's role. Someone needs to implement AI tools, train staff, oversee automated processes, and handle exceptions. Accountants with technical fluency are positioning themselves to own this space.

Specialization is accelerating. As routine work gets automated, generalist roles compress while specialist positions—forensic accounting, sustainability reporting, international tax, data analytics—become more valuable.

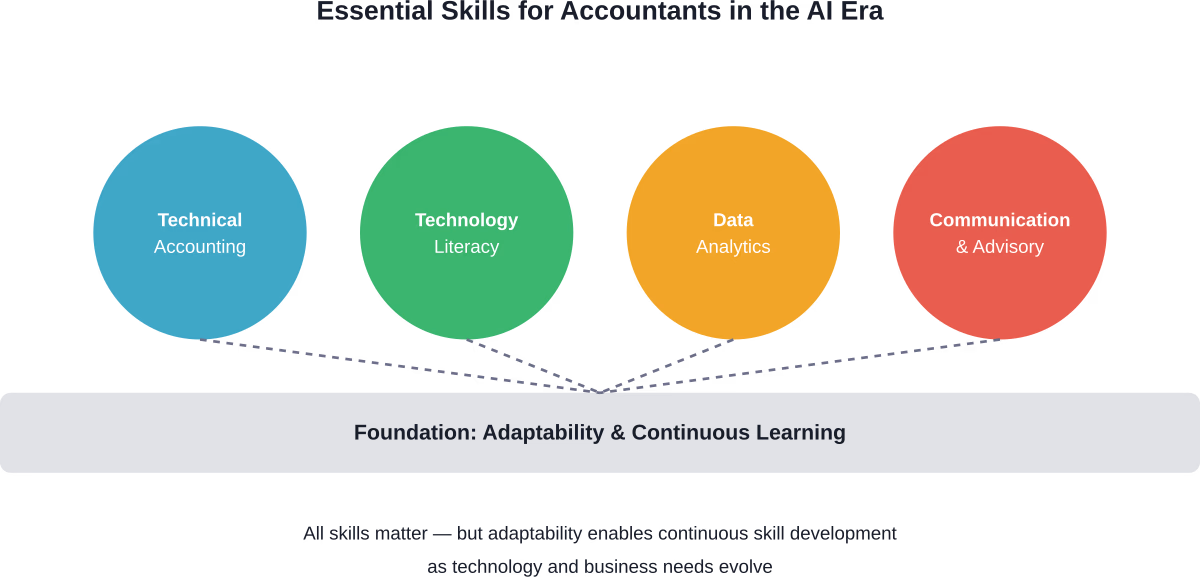

If the role is changing, required skills are changing too.

Technical accounting knowledge remains foundational. Understanding GAAP, IFRS, tax regulations, audit standards—these aren't going anywhere. But they're no longer sufficient by themselves.

Technology literacy has become essential. Accountants don't need to code necessarily, but they do need to understand how AI tools work, what their limitations are, when to trust automated outputs, and when to dig deeper.

According to research from NC State's Poole College of Business, workers in finance and accounting will need strong AI skills, critical thinking, interpersonal skills, and technical knowledge. That combination—not technical knowledge alone—defines future-ready accountants.

Data analytics capabilities are increasingly valuable. The ability to work with large datasets, identify patterns, visualize information, and translate data into business recommendations differentiates higher-level accountants from those doing routine work.

Communication skills matter more as advisory work expands. Explaining complex financial information to non-financial stakeholders, building client relationships, presenting recommendations persuasively—these soft skills become differentiators.

Adaptability might be the most important skill of all. Technology keeps evolving. Regulations change. Business models shift. Accountants who continuously learn and adapt will thrive; those who resist change face steeper challenges.

Major accounting firms have weighed in publicly on AI and the future of the profession.

The Big Four firms—Deloitte, PwC, EY, and KPMG—consistently emphasize that AI will not replace accountants. According to NYSSCPA sources, these firms agree that technology augments rather than replaces human professionals.

That stance aligns with their actions. Major firms are investing heavily in AI tools while simultaneously hiring accountants at scale. If they genuinely believed AI would replace accountants, hiring patterns would look different.

What these firms emphasize is transformation, not replacement. Finance teams need to move from cost centers to value centers, from historical reporting to forward-looking guidance, from transaction processing to strategic partnership.

Professional organizations echo this perspective. The American Institute of CPAs (AICPA) highlights that technology creates capacity in the finance function, but capitalizing on this requires the right skills and competencies.

So if AI won't replace accountants wholesale, what risks do exist?

Lower-skilled positions face compression. Basic bookkeeping roles that involve primarily data entry and routine transaction processing are most vulnerable to automation. Workers in these positions need to upskill or risk displacement.

Generalists without specialization may struggle. As routine work gets automated, demand concentrates on specialists who bring deep expertise in specific areas. Broad but shallow knowledge becomes less marketable.

Resistance to technology adoption creates career risk. Accountants who refuse to learn new tools, who cling to manual processes, who view AI as a threat rather than a tool—these professionals will find opportunities shrinking.

Small and mid-sized firms face competitive pressure. Large firms can invest more heavily in AI implementation, potentially creating service quality and efficiency gaps that affect smaller competitors.

But wait. These risks aren't about AI replacing accountants. They're about some accountants being better positioned than others to adapt to changing technology and client expectations.

Practical steps exist for accountants looking to remain relevant and valuable as AI reshapes the profession.

Embrace AI tools actively. Learn the software the firm uses. Experiment with generative AI for tasks like contract summarization or research. Understand what AI does well and where it fails.

Develop advisory capabilities. Take courses in business strategy, financial analysis, or industry-specific topics. Practice translating financial data into business recommendations.

Pursue specialized credentials. A CPA license improves job prospects according to the Bureau of Labor Statistics. Consider additional specializations in areas like forensic accounting, valuation, or IT audit.

Build technical and analytical skills. Learn Excel at an advanced level. Get comfortable with data visualization tools. Understand database concepts even if not coding directly.

Cultivate client relationship skills. Practice explaining complex topics simply. Develop emotional intelligence. Build networks within industries served.

Stay current on regulatory and technology changes. Read industry publications. Attend conferences. Join professional associations. Continuous learning isn't optional anymore.

AI technology continues advancing rapidly, which raises questions about what comes next for accounting.

Generative AI capabilities are expanding beyond current applications. Tasks that seem complex today may become automatable tomorrow. The line between automatable and non-automatable work will keep shifting.

According to the Bureau of Labor Statistics, AI is expected to primarily affect occupations whose core tasks can be most easily replicated by generative AI in its current form. But that form keeps evolving.

Integration across business systems will deepen. AI won't just automate individual tasks—it'll connect data across procurement, inventory, sales, HR, and finance to enable real-time visibility and predictive capabilities.

Regulatory frameworks will develop around AI use in accounting. Standards for AI audit trails, explainability requirements, accountability structures—these are coming and will shape how AI gets deployed.

New roles will emerge. AI ethics officers for finance functions. Technology implementation specialists. Data stewards. Some of these jobs don't exist yet, but accountants will fill many of them.

The profession won't look identical in ten years. But it won't disappear either. It'll evolve, as it has through previous waves of technological change.

Real talk: AI isn't replacing accountants. But anyone who thinks accounting work will stay the same is missing what's happening.

Routine tasks are getting automated aggressively. That creates both opportunity and risk depending on where individual accountants sit skill-wise and career-wise.

The profession is shifting from transaction processing toward advisory and strategic work. That shift rewards accountants who develop analytical capabilities, technology literacy, specialization, and client relationship skills.

Employment projections from authoritative sources like the Bureau of Labor Statistics show continued demand for accounting professionals, with specialized credentials improving prospects.

What matters most isn't whether AI will replace accountants—it won't. What matters is whether individual accountants will adapt to the changing nature of accounting work.

Those who embrace technology, develop high-value skills, specialize strategically, and focus on areas requiring human judgment will find expanding opportunities. Those who resist change and cling to routine work will face compression.

The future of accounting isn't humans versus machines. It's humans working with machines, each doing what they do best, creating more value together than either could alone.

That future is already here. The question isn't whether to adapt—it's how quickly.